In an era of rising card fraud and data breaches, financial institution leaders are constantly analyzing how they are protecting themselves, and their customers. One of the biggest problems today? Waiting for network alerts can be costly in terms of fraud loss and customer experience.

When relying on network alerts, by the time the information about fraud or a breach is realized, the amount of fraud loss and compromised card fraud can reach high levels. That’s where the power of fraud analytics, big data and machine learning comes into the mix. Financial institutions are getting faster and better at preventing, detecting and stopping fraud, thanks to help from more sophisticated software. But fraudsters are getting faster.

It’s no secret that AI, machine learning and big data are going to transform how financial institutions protect their customers from the influx of card fraud that continues to rise each year. Fraud and fraud patterns are evolving and change more rapidly than financial institutions can keep pace with. That’s where better data analytics tools bridge the gap by helping financial institutions detect breaches, risk and fraud faster, and at their source.

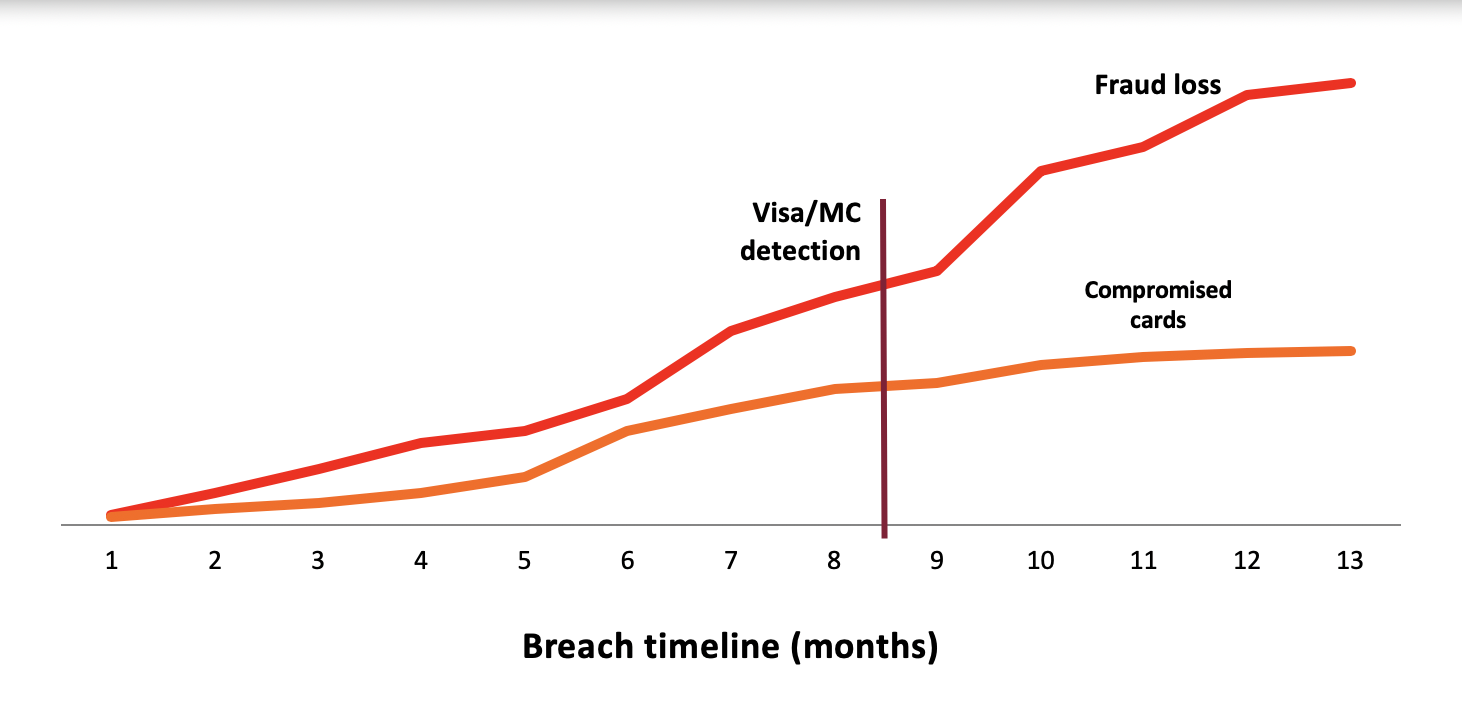

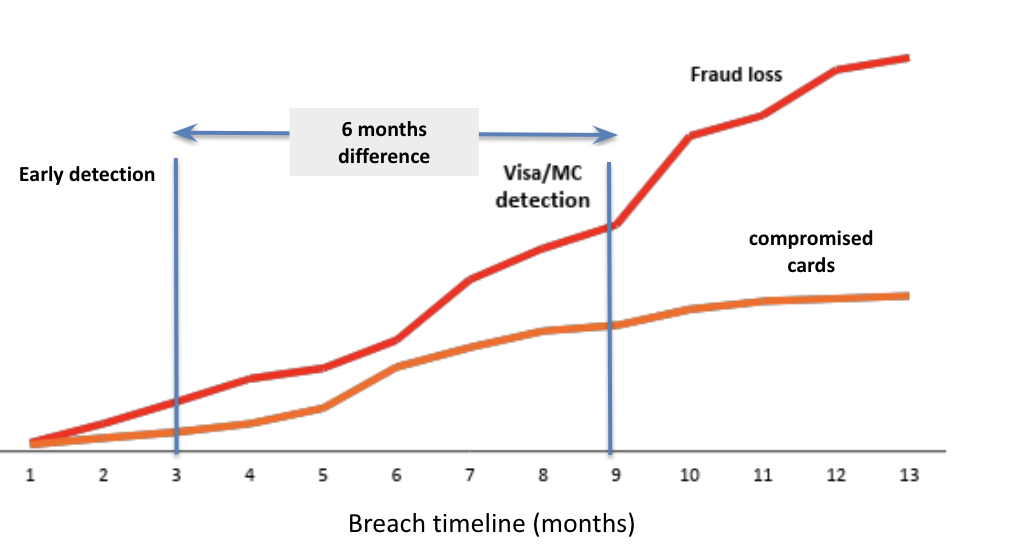

Without proactive tools to mitigate the risks associated with data breaches, this is the result.

Proactively mitigating risk is a no-brainer for any financial institution leader, but there are a few key issues that often prevent financial institutions from adequately solving this problem.

- Lacking Access To Adequate Big Data: Most financial institutions on’t have enough data to fight fraud effectively as it is not easily accessible

- Privacy Challenges: Consumer and personal identifiable information is very sensitive to financial institutions

- Lacking Resources: Financial institutions can be strapped for IT resources making technology implementation challenging

- Making Data Actionable: Data analytics need to be clearly actionable and deliver measurable ROI results

- Keeping Pace with Algorithms: Fraud and fraud patterns evolve and change more rapidly than financial institutions can keep pace

How a Big Data, Machine Learning Approach Gives Financial Institution Leaders an Edge

Fraud and fraud patterns are evolving and change more rapidly than financial institutions can keep pace with. This is where the value of machine learning and data analytics comes into the mix.The very nature of Machine Learning is to learn from the data it is processing, adapting to changing trends or relationships in the data. Detecting and mitigating fraud to manage risk involves in-depth data analysis to identify relationships and trends to pinpoint where and when the fraud originated. This includes Common Point of Purchase (CPP) analysis.

Relationships and trends are becoming leading indicators of outcomes (like fraud). As these leading indicators emerge in new data, outcomes can be predicted and acted upon. A data analytics approach equips issuers with the tools to understand what’s happening across their own card portfolio — and how to detect risk. But you have to have access to that data and be able to make sense of it all.

CPP analysis is a great example of how financial institutions can leverage data to determine where breaches may have happened and then take action. By using sophisticated data analysis, machine learning and algorithms to identify relationships and trends in transaction and fraud data. Those relationships and trends identify leading indicators of certain outcomes.

How Proactive Data Analytics Deliver Early Breach Detection

Early breach detection can stop 60% of fraud losses while reissuing less compromised cards. By using machine learning and big data analysis tools, credit union leaders can be better equipped to understand these relationships and trends as leading indicators of certain outcomes. As these leading indicators emerge in new data. Rippleshot, for example, is able to use old data to ID these relationships and trends, and applies those learnings to new data to start to predict certain outcomes and act on what the data is telling us is likely to happen.

Embracing Technology Advancements and Data-Driven Insights

Financial institutions have long relied on customer-centric approaches that insert too many manual review processes into the mix when attempting to track, detect and stop the spread of card fraud. This is particular true when analyzing card data. Within each transaction there are droves of data and information that can lend itself to the studying of spending habit patterns. This rich data can be used to study the path of fraudsters’ behavior, predict the spread of fraud and halt massive data breaches from occurring.

Banks can not longer overlook the value of faster, better card fraud detection as an element of customer service. The rise of data breaches has created an even great need for more software technology investments.

Insert the value of machine learning, data analytics and AI. Rather than waiting on manual review processes, or for alert systems to provide reports in a few weeks, banks should be demanding more in their card fraud compromise detection solutions. Automation is the future of fraud detection and banks should be embracing opportunities with more sophisticated technology in the market.

Solutions need to be able to streamline the data feed process, automate the analytics process, offer continuous model refresh, and deliver actionable results within hours — and continue to do so on a daily basis. Successful machine learning solutions for financial institutions automates the tasks of gathering and checking data, detecting fraud, and validating the results. This frees managers to make strategic decisions, as opposed to getting mired in the mechanics of machine learning.

Deployed properly, machine learning that continuously sifts through millions of transactions and variables to deliver timely results can help financial institutions better and more cost-effectively address the growing card fraud problem. As financial institutions continue down their digitization transformation — and invest in innovative technology — this opens the floodgates for more touch points for fraudsters to breach, particularly as it relates to card fraud.

Card fraud and data breaches are rising at alarming rates, causing issuers to spend thousands each month reissuing cards, investing in new fraud prevention tools and combating new market threats. With more sophisticated tools at their disposal, fraudsters are evolving as fast, if not faster than banks and payment networks. Thanks to machine learning, the digitization of data and artificial intelligence, financial institutions have access to the infrastructure and tools necessary to fight fraud — if they’re willing to invest money where it counts.