Just a few short months ago, NACHA put in motion a multi-year multi-phase plan to make ACH payments settle in the same day they’re originated. This past September, ACH credits were first made available for same day settlement, with the receiving depository financial institution (RDFI) making the funds available by the end of their processing day. In phases two and three of this rollout, debits will also be settled same day, and funds made available at 5:00pm local time for the RDFI. It goes without saying that as the time available to settle payments decreases, the opportunity for fraud increases, but it’s also important to understand what exactly “same day” means, what opportunities for fraud detection are available, and what the landscape for ACH fraud looks like moving forward.

Just a few short months ago, NACHA put in motion a multi-year multi-phase plan to make ACH payments settle in the same day they’re originated. This past September, ACH credits were first made available for same day settlement, with the receiving depository financial institution (RDFI) making the funds available by the end of their processing day. In phases two and three of this rollout, debits will also be settled same day, and funds made available at 5:00pm local time for the RDFI. It goes without saying that as the time available to settle payments decreases, the opportunity for fraud increases, but it’s also important to understand what exactly “same day” means, what opportunities for fraud detection are available, and what the landscape for ACH fraud looks like moving forward.

What Does “Same Day” Really Mean?

Well, it’s not instant, but it’s certainly closer than we’ve ever been. NACHA has outlined two new clearing windows provided by the ACH operators (which are FedACH and the Electronic Payments Network [EPN]). The windows work as follows:

Morning deadline: 10:30 AM ET, with settlement occurring at 1:00 PM.

Afternoon deadline: 2:45 PM ET, with settlement occurring at 5:00 PM.

Though this makes money available to consumers within hours, what makes this faster settlement difficult is that the time available for review is significantly shrunk, and once completed, transactions are hard to reverse.

As Ruston Miles, founder and chief innovation office of Bluefin Payment Systems told LowCards.com, “Anytime you push money out, it’s really hard to pull it back. If it’s a payroll file, the money has been pushed out, and you can’t go out to the customer and pull it back.”

What Do Fraud Detection and Prevention Efforts Look Like?

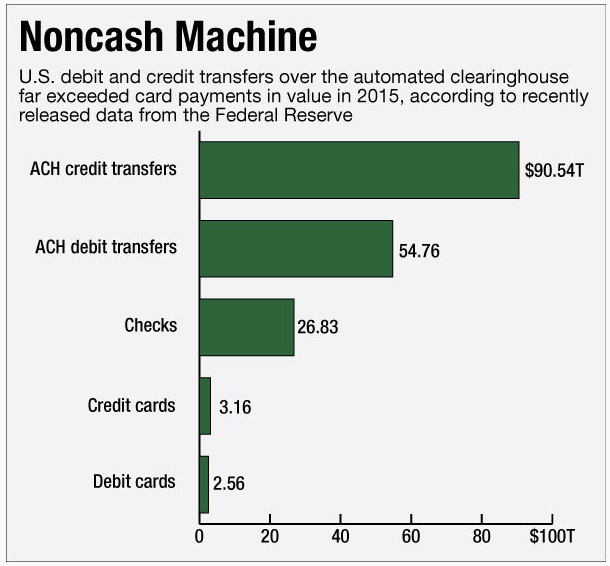

As noted in American Banker, a Federal Reserve study revealed that ACH credit transfers overwhelmingly exceeded ACH debit, checks, credit and debit transfers in value in 2015.

This should have painted an enormous target on ACH credits for fraudulent attempts - but as any good criminal knows, time is of the utmost importance, and the former system just didn’t lend itself to quickly moving money illegally.

This should have painted an enormous target on ACH credits for fraudulent attempts - but as any good criminal knows, time is of the utmost importance, and the former system just didn’t lend itself to quickly moving money illegally.

Up until this point, RDFIs had until the next business day to settle ACH transactions, which left at least some time to review suspicious-looking transactions and call customers to confirm. With settlements now happening within a matter of hours, it’s getting more and more difficult to continue this manual process of having a person review flagged transactions.

Most current systems have something in place to flag transactions that don’t look “right,” but most aren’t employing tools that can run comprehensive checks on the history of the originating and receiving accounts in order to determine the relative risk.

And in the case of something like payee fraud, where a criminal is changing the destination of something like a payroll file, it’s rare that something or someone at the bank is reviewing the validity of every single receiving account each week to make sure they weren’t tampered with.

In the case of ACH credits, which payroll fits into, the funds are made available same day, and can be withdrawn same day - which as we mentioned above, makes reversing fraud nearly impossible.

As David Pollino, CSO for Bank of the West, stated in the American Banker article, there is a potential upside to faster payments - being able to “risk-stack,” knowing that faster offerings are more likely to see increased fraudulent attempts.

What’s the Fraud Landscape Look Like Going Forward?

Some would say that this same day initiative is nothing new, since there was always the option to pay more to accelerate an ACH transfer - which criminals certainly employed. However, it’s a different landscape when expedited payments are the norm, and not the exception.

While NACHA denies any knowledge of increased fraud, many individual banks are reporting otherwise. Unfortunately, there’s probably more to come.

When ACH debit begins same day settlement later this year, there is concern that bank account numbers, which we all have been pretty liberal in sharing (via checks, etc), could become much more valuable to fraudsters. Traditionally, card information has been more desirable, since it could be used quicker - but with same day ACH debit settlement coming soon, account and routing numbers may make a run up the list.

A Note From the Author

We’ve heard some anecdotal feedback from clients and partners who are worried about increasing ACH fraud, and a lack of solutions to address it. Are you looking for help, too? We’d love to learn more about how we can assist. Shoot us an email - info @ rippleshot.com - we’d be thrilled to hear from you!