No surprise here. Pulse Network’s 2016 Debit Issuer Study cites an across the board increase in fraud losses for all types of financial institutions from 2014 to 2015. But where’s it all coming from? How will mobile payments impact the debit market? And what sort of growth is expected over the coming years? We cover it all ahead:

Fraud Loss Rates

Financial institutions of all sizes suffered increases in fraud losses on no-PIN POS debit transactions from 2014 to 2015, with community banks suffering the biggest hit (from $.020 to $.031 per transaction). Overall, the industry saw a $.004 per transaction increase year over year. But what’s interesting is that even PIN POS debit transactions saw an increase in net fraud loss rates, with the industry overall seeing a 3x increase (from $.003 to $.008 per transaction) year over year.

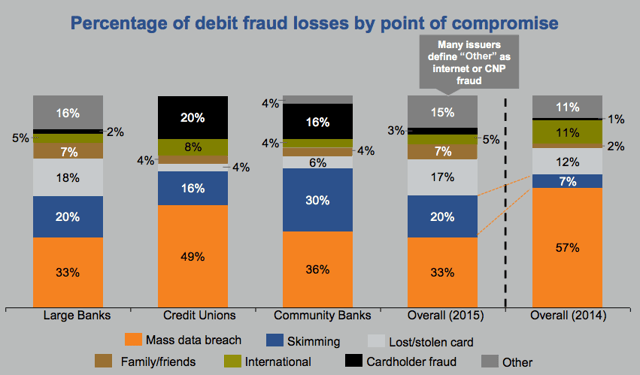

Debit Card Fraud Sources

The root of debit card fraud has changed pretty considerably from 2014 to 2015, with skimming, lost/stolen cards and other (which often includes e-commerce/CNP) fraud all seeing increases. Mass data breaches are still responsible for roughly one-third of all debit card fraud, and skimming (like we’ve covered here) is now responsible for 20%.

Credit unions seem to be disproportionately affected by mass data breaches, with 49% of their debit fraud losses coming from this source. Likewise, community banks take a unusually high loss from skimming incidents (as compared to their peers) with 30% of their losses coming via these incidents.

Why This is Still an Issue

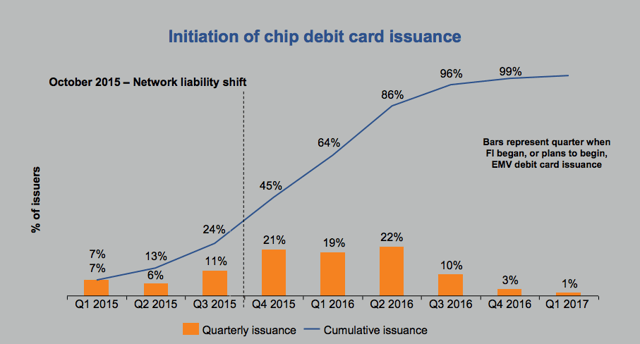

Of all debit transactions in 2015, 64% were magnetic stripe cards used at non-chip terminals. Another 32% were chip card transactions made at non-chip terminals, which leaves only a very small percentage - 4% - that were made with chip cards at chip terminals. But, this isn’t incredibly surprising, considering that the EMV shift took place toward the end of 2015 and we knew implementation, especially on the merchant side, would lag. What’s more important to look at is the expected penetration of chip cards moving forward.

At the time of the shift, only roughly 20% of issuers had initiated chip card issuance. By the end of this year, 99% of issuers are expected to begin the issuance of chip cards, though we doubt we’ll see that level of actual chip debit cards in consumers hands for many months, if not years, to come.

Issuers echo these sentiments, as they only anticipate 76% of debit cards to be converted by the end of 2016, even though almost all issuers will have initiated the process. That number jumps to 91% in 2017, and is expected to reach close to 100% by the end of 2018.

Mobile Payment Expectations

While the current adoption rate is low, with Apple Pay, Samsung Pay and Android Pay collectively processing .19% of debit transactions in January 2016, the expectations for future adoption are much more optimistic than in years past.

In 2014, only 30% of issuers surveyed felt that more than 25% of transactions would move over to mobile in the next five years. This year’s study saw that number jump to 46%. Cardholders are having an overall positive experience with speed and security, and issuers enjoy the ease of implementation and servicing mobile payments. The biggest issue that plagues mobile adoption is the difficulty in authenticating users, which has resulted in very high call volumes for banks and credit unions. We covered this problem with Apple Pay back when it first launched nearly two years ago, but it continues to plague the onboarding process.

2016 Challenges

Not much has changed in this arena. Just as in 2015, fraud and regulation remain the top challenges for issuers, with a new issue breaking into the top three this year - keeping up with emerging financial technologies. The team here at Rippleshot pride ourselves on staying on the cutting edge of financial technology, while tackling issues that matter - like fraud. To learn more about our recently ABA-endorsed solution, Sonar, see below: