Financial institutions are continuing down their digitization transformation by investing in innovative technology. The problem? This opens the floodgates for more touch points for hackers to breach. Another problem? Those fraudsters are more sophisticated than ever. Banks are using new tools to fight fraud— machine learning, automation, cloud technology, etc. — but so are the fraudsters.

It's a bit of a Catch 22 that exists within the card fraud ecosystem.

Credit card fraud is a rapidly-growing problem impacting businesses and financial institutions of all sizes — and the problem is only getting worse.

In our State of Card Fraud 2017 whitepaper, we explore evolving threats, emerging fraud trends, new EMV updates, ATM fraud and how banks and credit unions can benefit from integrating machine learning technology to enhance their card fraud management.

The monetization of compromised cards has become a sophisticated industry. As a result, payment credentials are getting increasingly tangled in this fast-growing problem as more vulnerabilities are exposed across the ecosystem (as new technologies enter the market).

Six Key Facts from the State of Card Fraud 2017

- Nearly 50% of all the credit card fraud around the world occurs in the U.S., despite the fact that the U.S. accounts for only about a quarter of the global card volume.

- According to a Nilson report, plastic card fraud is expected to grow to $31.67 billion in 2020. That’s a 42 percent increase.

- Data from the across the industry indicates that just over half (57 percent) of U.S. merchants are EMV-equipped to accept chip cards.

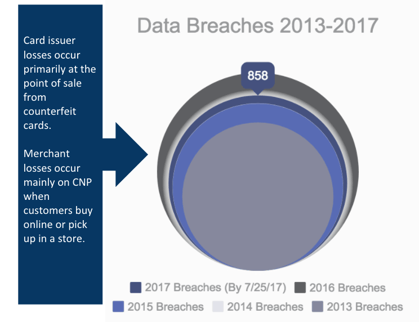

- The ITRC projects breaches to hit 1,500 in 2017 (37% YOY increase).

- Synthetic ID fraud accounts for 80% of all credit card fraud losses, and nearly one-fifth of credit card charge-offs.

- By the time networks alert banks which cards are comprised, 80% of fraud has already occurred.

Banks and credit unions are faced with many challenges today in a financial ecosystem filled with more wide-reaching breaches and increasingly sophisticated hackers. With card fraud growing at a record-setting pace every year, it is expected to be a $35 billion problem by 2020. And financial institutions are continuing to feel the pinch.

As we mentioned, fraudsters are getting more sophisticated with their techniques, using bigger data sets and gaining access to far more than just social security numbers, emails, addresses and birthdates. Payment credentials are getting increasingly tangled in this fast-growing problem as more vulnerabilities are exposed across the ecosystem (as new technologies enter the market).

The state of Card Fraud and the Promise of Machine Learning

Rippleshot’s team discovered that over 50 percent of fraud that’s not being caught was correlated to data breaches. While many banks have fraud teams trying to tackle this problem alone, taking a manual approach to fraud detection isn’t sophisticated enough for today’s data breach-filled ecosystem. With so many innovations in the marketplace, banks shouldn't have to manage the cost of fraud alone.

As we’ve explored in previous posts, machine learning technology already has the power to transform the financial services industry in ways not possible before. Luckily, this technology allows banks to thwart off breach threats faster, detect breaches when they occur, and devise a plan of attack for when breaches hit — preventing them from spreading into even bigger problems.

Thanks to machine learning, the digitization of data and artificial intelligence, banks and credit unions have access to the infrastructure and tools necessary to fight fraud — if they’re willing to invest money where it counts.

Regardless of new innovations to the marketplace, it will take time to build that infrastructure and learn those new skills – which means card fraud will continue to get worse before it gets better. However, proactive organizations that have invested in people, the power of big data, and technology like machine learning can achieve dramatic success in reducing fraud.

What can you do to stay ahead of this problem — and proactively manage your fraud mitigtation strategies? Check out ourState of Carc Fraud 2017 whitepaper for more insights from our team.